Oil Giants Burnt by Chavez Eye Venezuela’s New Black Gold Rush

Dealmakers are scrambling to secure supplies after Trump captured Maduro, but despite Venezuela having the largest proved reserves on Earth, it’s not as simple as turning on the taps.

Don’t miss yesterday’s vital Deep Dive on America’s new Asian security architecture.

by Hans van Leeuwen

May 13, 2026

A week after U.S. troops spirited then-president Nicolas Maduro out of Venezuela in early January, the boss of ExxonMobil told Donald Trump that the oil-rich, dirt-poor country was “uninvestable”.

It didn’t take him long to change his tune.

“Venezuela is a huge resource that’s now opened up more freely to the world,” Darren Woods, Exxon’s chief, said in late April after dispatching a technical evaluation team to the country. “I feel positive about what’s happening, the opportunity there.”

He’s not the only one.

The Courts have taken liberties with the Constitution for far too long. An Article V convention could close the loopholes. Learn more here.

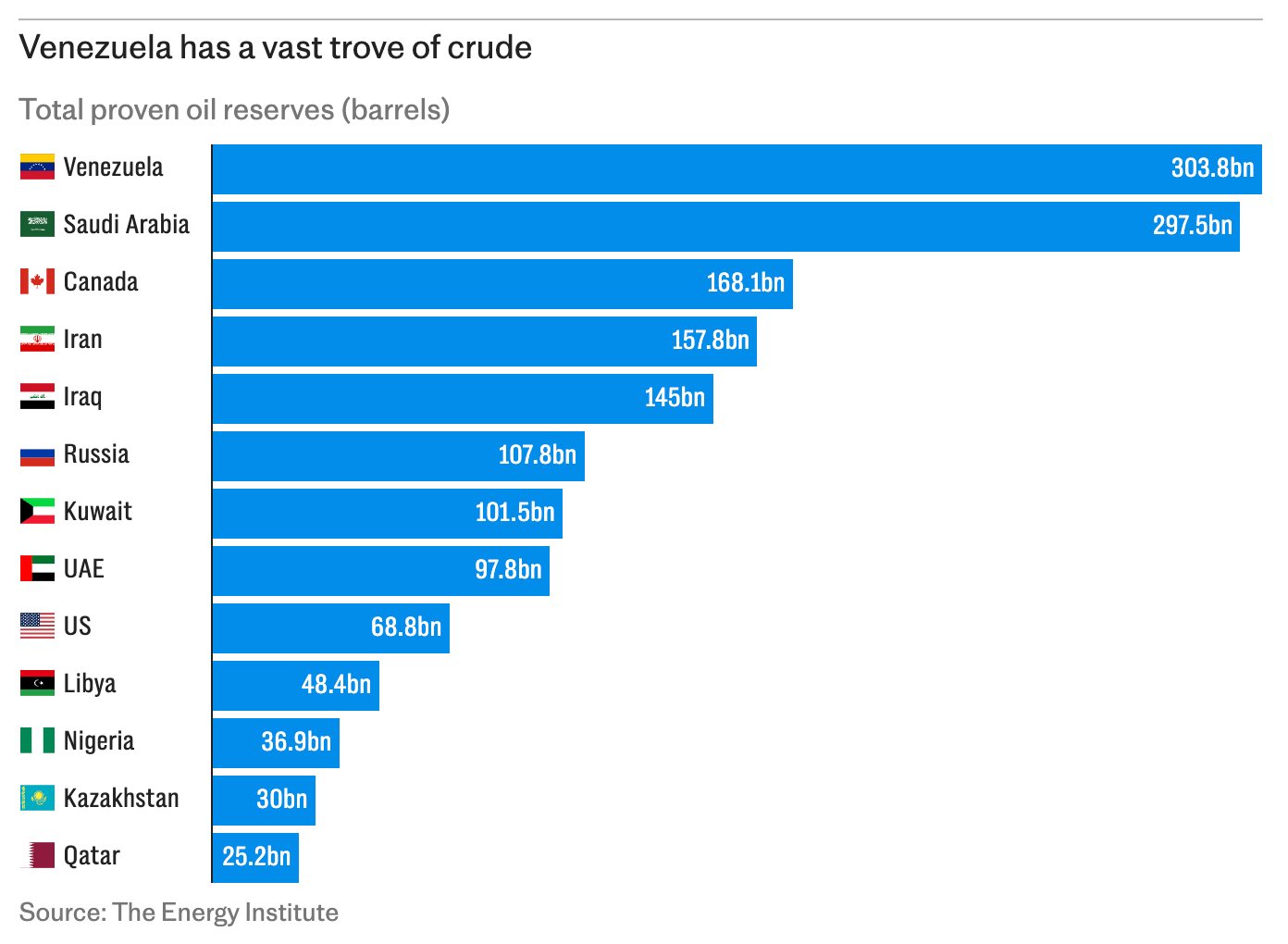

Oil industry dealmakers have been schmoozing with U.S. politicians and jetting into Venezuela’s capital, Caracas, in recent weeks to get ahead in the scramble for its black gold. The country has the biggest oil reserves in the world, but American sanctions against the anti-U.S. Maduro regime left the country largely off-limits to most of the global oil giants, while socialist ineptitude cut the country’s production to a fraction of before.

Many oil majors also carry lasting scars from a decade earlier, when Maduro’s predecessor, Hugo Chávez, seized their assets. Several companies are still owed billions of dollars.

But now the Caracas JW Marriott hotel, which hosts a makeshift U.S. embassy, is crawling with oilmen. Chevron, BP, Shell, Repsol, Eni, ExxonMobil and ConocoPhillips have joined a host of smaller rivals all looking to get in early as Trump reopens Venezuela’s moribund oil and gas industry to foreign players.

Trump himself is reveling in the Venezuelan oil rush.

“I was with ExxonMobil last night. The president of the company was here. And we were talking about Venezuela. [...] Chevron was all here last night. They all want to go there,” he said in Washington last week.

“It’s been a great thing for Venezuela. People are really happy. They’re dancing in the streets because there’s a lot of money coming in through the big oil companies that are moving in there.”

Venezuela’s new president, Delcy Rodríguez, will only hold on to her post if she delivers Trump’s demand for quick and open access for the oil companies. Unsurprisingly, she’s rolling out the red carpet. But she sits atop a largely unreconstructed regime, built on the same politicians who terrorised their political opponents and ran the economy — and the oil industry — into the ground.

Nobody can yet be sure if she and the Trump administration can reform and rejuvenate Venezuela. The oil execs worry that corruption, factional infighting, vested interests and incompetence could send the country spiralling back down, particularly if Washington becomes distracted elsewhere.

Rodríguez, who was oil minister under Maduro, has rolled the pitch with a new hydrocarbon law. This gives the oil giants greater control of their operations in the country, halves their royalty bills and bolsters the process of dispute resolution.

But the regulatory fine print is yet to be nailed down, leaving the oil companies waiting for clarity about how safe their money will be. The hydrocarbon law “moves things in a positive direction”, Mike Wirth, the boss of Chevron, told CBS News. “It still needs some work, it’s probably not enough to bring in the level of investment that would be desirable.”

What has prompted the companies to throw some of their caution to the wind, though, is the upheaval of the Iran war.

“It’s very difficult to ignore Venezuela in the context of the Iran war. Not only because of the price dynamics and the supply shortages, but also because of the lessons learned about diversification of suppliers, and diversification of risk,” says Luisa Palacios, of Columbia University’s Center on Global Energy Policy.

With oil prices high and supply chains broken, there’s a push to get Venezuelan crude into the Gulf of America’s refineries as quickly as possible.

Chevron, which remained in Venezuela when most others pulled out, has stepped up its interest quickly. It has conducted an asset swap with the state-owned oil company Petróleos de Venezuela (PDVSA). This has boosted its rights to exploit some oilfields, and increased its equity stake in its Petroindependencia joint venture to 49 percent.

Similarly, Spain’s Repsol has signed a deal to resume control of its Venezuelan oil assets. It aims to boost its crude output from those projects by 50 percent within 12 months and to triple it over the next three years. It will also step up gas production by 10 percent.

PDVSA still owes Repsol almost $4.6bn, although Josu Jon Imaz San Miguel, its chief executive, is hopeful that Venezuela’s re-opening will increase the possibility of repayment. “I’m sure that we are going to find windows of opportunity to talk and to try to address this question,” he said.

Shell has also inked deals with the new regime to look at oil and gas developments. The priority is a plan to pipe gas from the Dragon offshore field to its liquefied natural gas plant in nearby Trinidad & Tobago.

Other projects “will take quite some time to gestate”, Sawan Wael, the Shell boss, warned investors.

Elsewhere, ConocoPhillips is still owed about $12 billion from Chávez’s expropriation of its interests in the early 2000s. So far, it has sent an evaluation team to “better understand the potential for in-country oil and gas opportunities”.

BP has signed a memorandum of understanding on “potential areas for co‑operation in material offshore gas and future exploration”.

Italy’s Eni is also weighing up the next move for its Venezuelan offshore oil and gas interests. Its chief, Claudio Descalzi, was in Caracas at the end of April, meeting Rodríguez and the PDVSA top brass.

However, the flurry of oil chiefs dropping by the presidential palace in Caracas does not yet mean that serious money is pouring in, Palacios warns.

“The companies are saying, ‘What has happened is enough for us to start the conversation, to start to consider the investments’. It’s not yet a done deal,” she says.

“Right now I see a lot of spending that can be recovered fast. A lot of scaffolding still needs to take place, to translate significant interest and announcements into actual investments.”

One oil exec admits as much: “Everything seems to have gone really quickly, and there’s a lot of expectation, but on the ground things are not moving so fast,” he says. “It’s moving more quickly than expected, yes, but not as fast as the U.S. administration would like.”

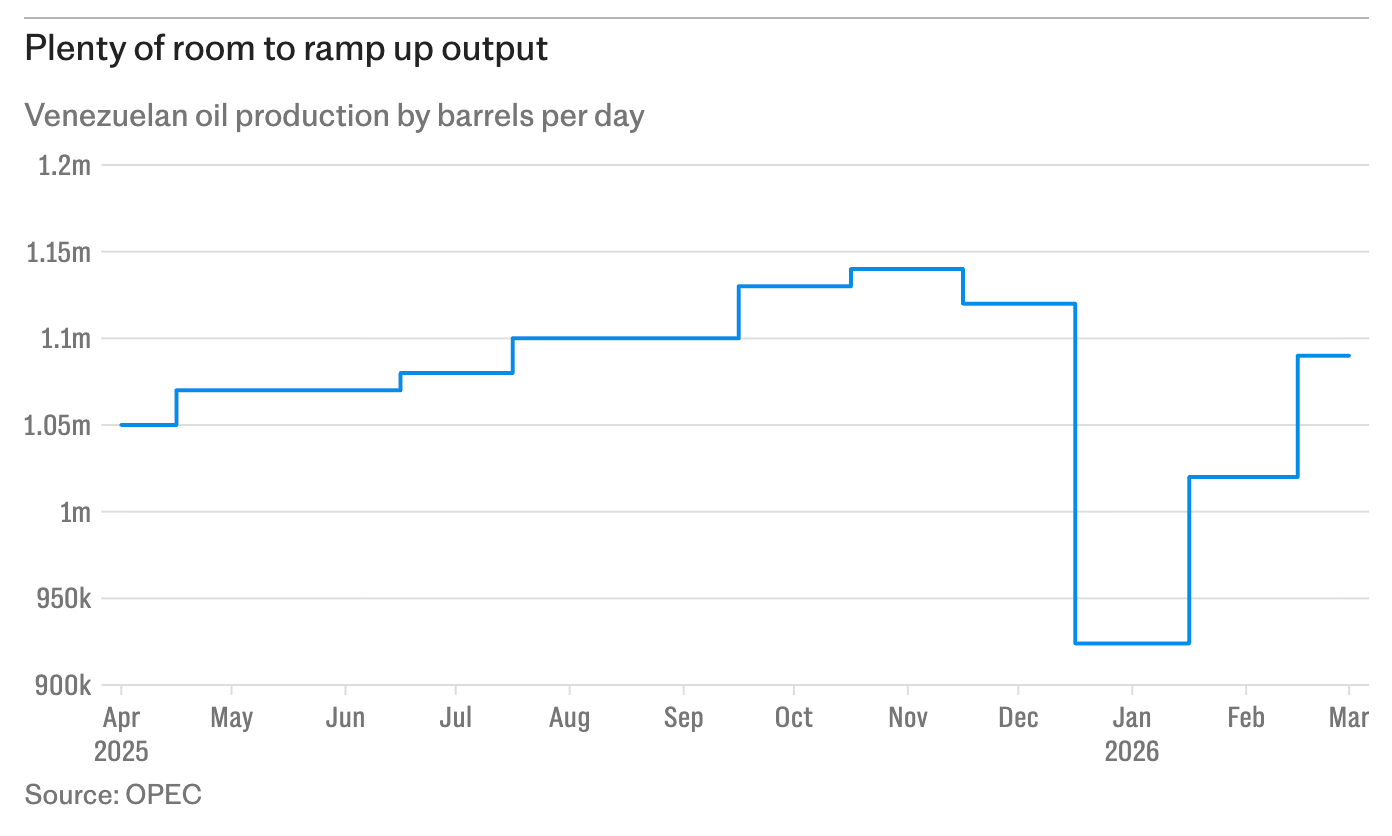

Before the socialist revolution, Venezuela produced 3.5 million barrels per day. But under Chavez and Maduro’s regime, that number dropped to as little as 500,000 bpd. In recent years it recovered to 800,000-1.1 million bpd, still a small fraction of its pre-socialist past.

Palacios says oil companies need to see the rule of law taking root, so they can be sure their investments are protected this time.

Yet this might not necessarily mean a shift to democracy, says Caracas-based Phil Gunson, of the International Crisis Group. “If what the U.S. really wants is a friendly Venezuelan government open to US businesses, then it’s already got a large part of that,” he says.

The Trump administration says elections and a democratic transition are part of its plan, but it is wary of repeating the chaos of Iraq. “Political transitions are complicated and difficult to manage. It’s quite possible to imagine that there could be a hard-line backlash to it,” says Gunson.

There is a more urgent task: fixing the country’s creaking infrastructure, which will cost tens of billions of dollars.

“It’s not a question of getting an oil concession, showing up with your workers and turning on the tap. All the infrastructure is seriously deteriorated,” Gunson says.

“It’s not just the oil installations themselves, but also rebuilding the electricity infrastructure. If you imagine an economy that starts to grow at 10 percent a year, say, the electricity industry simply couldn’t keep pace. And everything else, from roads to water to hospitals to the internet, is in a total mess.”

The rush to repair infrastructure could spark an economic surge, with some pundits predicting a construction boom that could fuel double-digit GDP growth this year.

Meanwhile, despite the dilapidation, more oil is already starting to flow. Since Maduro’s ousting, exports to the US have averaged more than 300,000 barrels a day — almost triple the rate of last year.

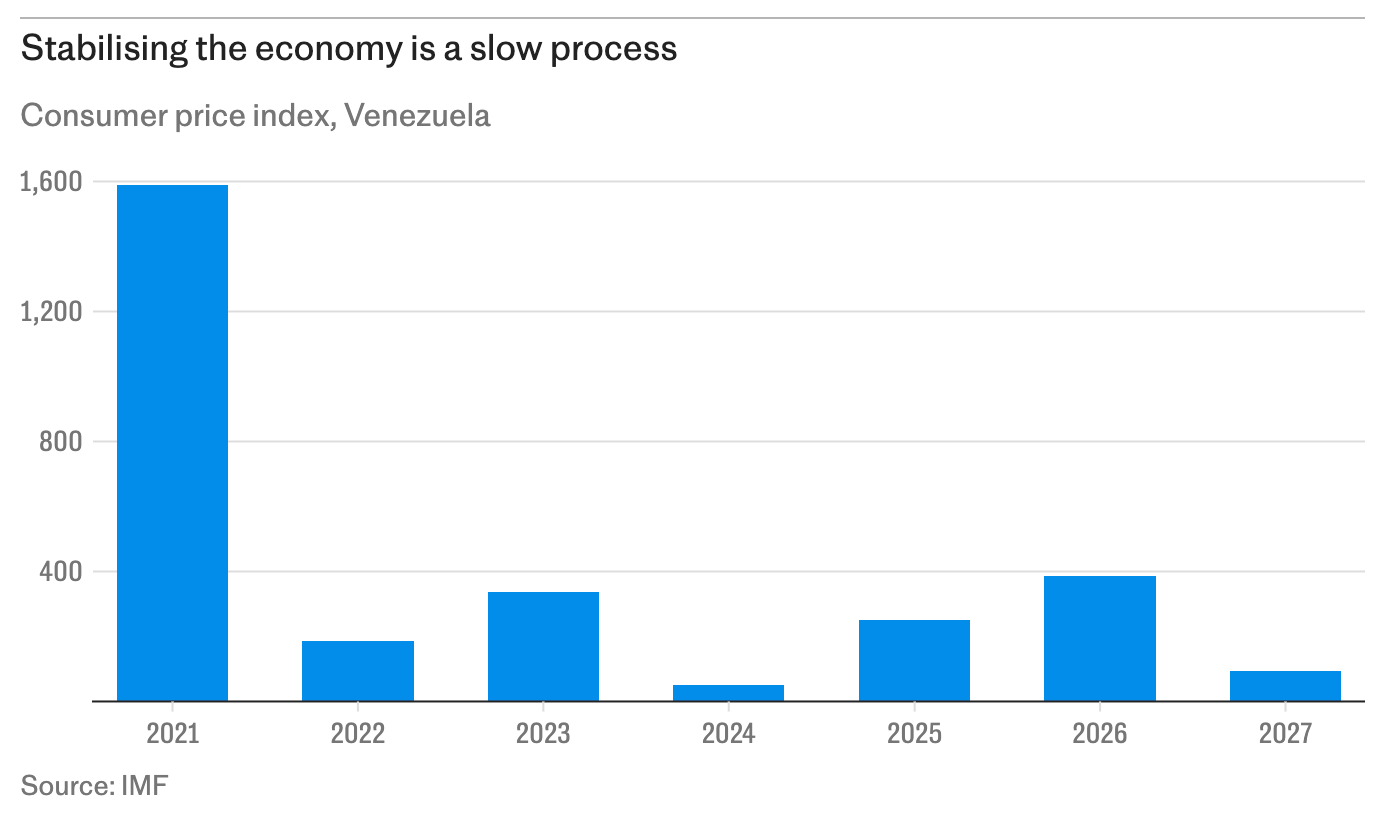

Venezuelans might not be dancing in the streets yet, but they could potentially see an easing in the country’s rampant inflation.

That may help Rodríguez in the short term. But she remains in office at the whim of the White House and under the threat of a looming election. In the last one, stolen by Maduro, the consensus of international observers was that the opposition won around 70 percent of the vote.

Regardless, hopes in Venezuela are far higher than seemed possible just a few short months ago.

— Hans van Leeuwen is International Economics Editor for The Telegraph, where this essay first appeared.

Venezuela doesn't have 303 billion barrels of reserves of heavy oil. The recovery rate in the Orinoco Belt is ~7%. With an estimated 1.3 trillion barrels of oil in place, that translates to about 90 billion barrels of reserves. Gotta get that recovery rate up to get the reserves number up.